The home furnishings industry continues to face significant headwinds, and Ethan Allen Interiors Inc. (ETD) remains firmly on the defensive. Persistent pressure from trade tensions, a sluggish housing market, and shifting consumer spending patterns has weighed on furniture and home decor demand, leaving little room for earnings growth.

Ethan Allen’s performance reflects these challenges. ETD stock has underperformed across multiple timeframes, lagging both its peers and the broader market over the past one, three, and ten years. Despite a brief post-pandemic rebound, sales have been essentially flat for several years, and recent quarterly results show no signs of meaningful acceleration.

Technically, the chart is deteriorating again, with shares appearing vulnerable to another breakdown. Fundamentally, the outlook has worsened as analysts have cut earnings estimates sharply in recent weeks, citing weak order trends and margin pressure. Yet the stock still trades at a premium to its historical valuation, leaving little cushion if conditions deteriorate further. For now, the risk/reward balance skews clearly to the downside.

Image Source: Zacks Investment Research

Ethan Allen Interiors Stock Gets Downgraded

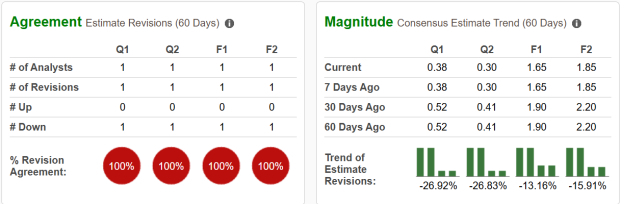

Ethan Allen Interiors has seen a wave of downward earnings revisions over the past week, with the pace of cuts accelerating. While estimates have been trending lower since late 2023, the declines have recently become more pronounced, with current quarter projections are down nearly 27%, and full year estimates have fallen 13.2%. As a result, the stock now carries a Zacks Rank #5 (Strong Sell) rating.

Valuation adds to the pressure. ETD currently trades at 14.3x forward earnings, a discount to the broader industry average but still well above its five-year median of 10.6x. Given the company’s weakening outlook and soft demand backdrop, this premium looks difficult to justify. Unless earnings expectations stabilize, the combination of estimate cuts and an elevated multiple suggests further downside risk for the stock.

Image Source: Zacks Investment Research

Shares of Ethan Allen Breakdown

The recent price action in ETD stock reflects its weakening fundamentals. After trading mostly sideways for the past two years, shares have now broken below a key support level, confirming a technical breakdown. The loss of this support aligns with the company’s deteriorating earnings outlook and accelerating analyst downgrades.

As long as the stock remains below that prior support zone, momentum favors the downside. Investors may want to stay on the sidelines until Ethan Allen shows signs of stabilization in both its fundamentals and chart pattern.

Image Source: TradingView

Should Investors Avoid ETD Stock?

Given the accelerating earnings downgrades, weak sales trends, and confirmed technical breakdown, Ethan Allen Interiors appears positioned for further weakness. The company’s elevated valuation leaves limited margin for error, and industry conditions remain unfavorable.

Until earnings stabilize and demand in the home furnishings market improves, investors are likely better off avoiding ETD and focusing on sectors with clearer growth catalysts and stronger momentum.

Quantum Computing Stocks Set To Soar

Artificial intelligence has already reshaped the investment landscape, and its convergence with quantum computing could lead to the most significant wealth-building opportunities of our time.

Today, you have a chance to position your portfolio at the forefront of this technological revolution. In our urgent special report, Beyond AI: The Quantum Leap in Computing Power, you’ll discover the little-known stocks we believe will win the quantum computing race and deliver massive gains to early investors.

Ethan Allen Interiors Inc. (ETD) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.